Last Week in Housing and Rates: A Snapshot

Courtesy of NEXA Mortgage

Last week brought market anticipation for the Fed’s upcoming rate decision this Wednesday, with a focus on its potential impact on rates heading into March. So let's expect a more active calendar with several relatively important reports in addition to Wednesday's rate announcement from the Fed. While the Fed will not be cutting rates at this meeting, the post-meeting press conference can still serve as a source of inspiration for rates.

There are several other considerations for rates beyond economic data. Given that Trump said he would "demand that interest rates drop immediately" this week, it's worth asking whether a president has a direct say in the matter.

In short, no... not directly anyway. Indirectly, the government and a presidential administration can have a massive impact on rates, but that impact is almost exclusively a result of changes in the economy and the government's borrowing needs.

The Role of Economic Data in Rate Movements

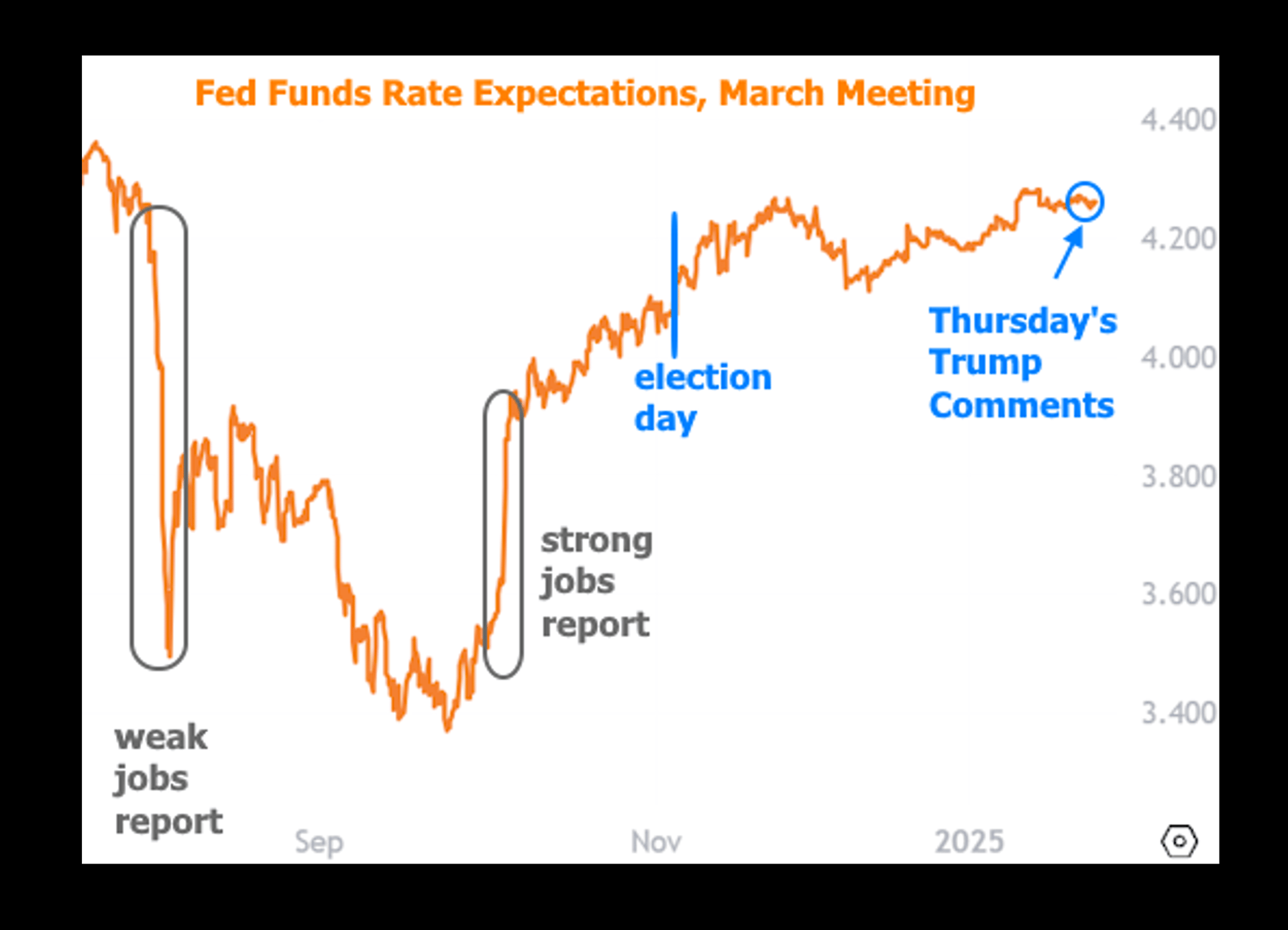

Jobs data, inflation reports, and political comments can significantly influence rate expectations. For example, recent Fed Funds Rate projections for March have fluctuated due to weak and strong jobs reports, as well as public statements from key figures.

What Lies Ahead

The Fed is designed to be independent and ideally, uninfluenced by political pressure. Traders (the people who will ultimately determine exactly how interest rates move) agree, as can be seen in the following chart of Fed Funds Futures. The chart shows where the market sees the Fed Funds Rate after the March Fed announcement (the next meeting with even a remote chance of seeing a cut).

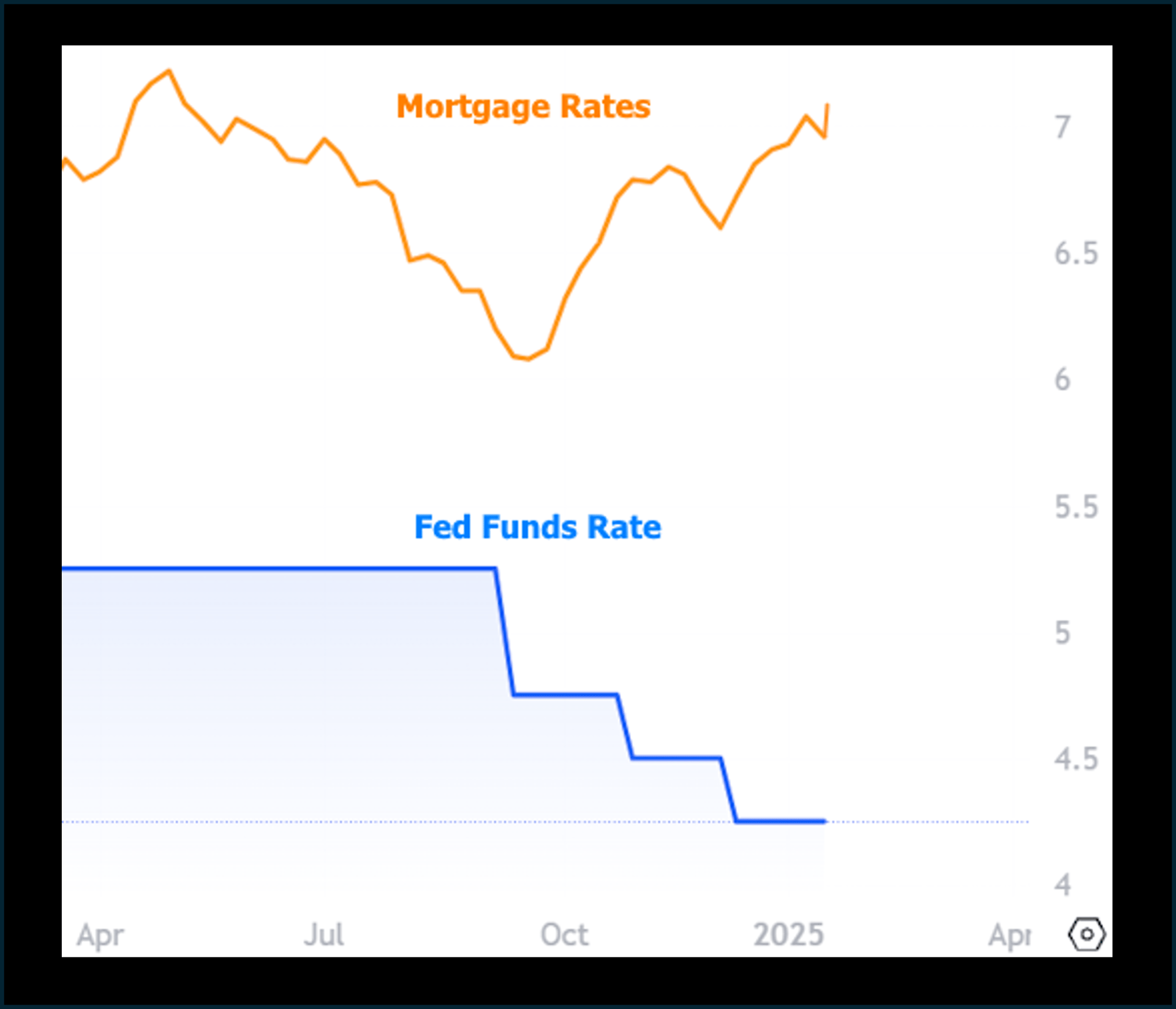

Even if mortgage rates were tied to the Fed Funds Rate, there's an inherent problem with unjustified Fed rate cuts. The entire point of a high Fed Funds Rate is to increase the cost of credit in an attempt to cool inflationary pressures in the economy. Dropping the rate prematurely or excessively would risk sabotaging progress toward inflation goals. If inflation were to increase, the Fed would have to increase the Fed Funds Rate in response.

Bottom Line

Even if the Fed Funds Rate would help mortgage rates (the chart above shows us how that's been working out), the fallout from cheaper credit would likely result in rates moving even higher in the future. The best hope for rates continues to be ongoing moderation in inflation data, a stable economy, and lower Treasury issuance.

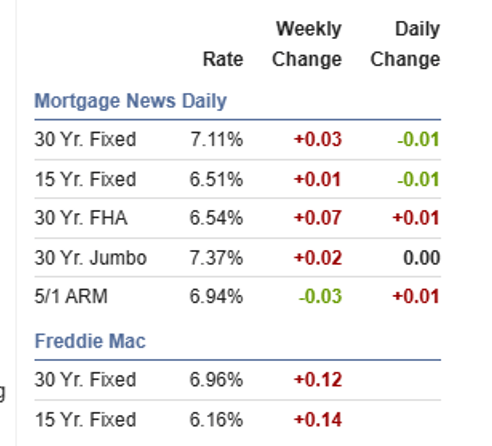

NATIONAL AVERAGE MORTGAGE RATES